Well, it didn’t take long for the equity markets to find a reason to decline from higher levels. As indicated in my posts on August 1st and July 31st, U.S. equity markets were close to resistance and peak levels, and that investors just needed some sort of shock for the equity markets to sell off from those levels.

The “shock”, which isn’t really a fundamental shock at all, is that Fitch Ratings, a company that rates the quality of various entities’ (governments, companies) debt, just downgraded the credit rating of long-term U.S. Treasuries from AAA to AA+. Just like any person who has a credit score, the U.S. government has a “credit score” as well, and it just declined in the eyes of a credit agency.

As a reminder, Standard & Poor’s (another credit rating agency) downgraded U.S. Treasuries from AAA to AA+ back in 2011. Yes, the equity market sold off and bond yields moved higher, but that was the first major ratings agency to downgrade U.S. debt, and was more of a short-term “shock” at that time.

Most investors (and probably non-investors know that the U.S. is incurring higher amounts of debt relative to GDP and it is an issue. We don’t need Fitch to remind us that. I also believe that if a U.S. investor is looking for safety in government bonds, I’m highly skeptical that they still won’t continue to invest in U.S. Treasuries. As long as the U.S. government doesn’t default on their bonds, which appears to be a low probability at this time, investors will likely consider it money good.

It’s All Relative

Here’s a quick check: If you want to invest in a government bond for 10 years, would you invest in 10-year U.S. Treasuries, or bonds issued by Germany? Canada? Brazil? The U.K.? Other foreign bonds can come with additional currency volatility as well. I think most U.S. investors seeking safety in long-term government bonds would prefer to continue investing in U.S. Treasuries relative to other foreign government bond options.

So for those who are expecting a huge spike in U.S. Treasury yields and a big sell off in bond prices relative to other government bonds, I think they will be very disappointed.

What investors need to remember, is that Treasury yields are based on what Treasury investors want to pay for the debt. It has very little to do with credit ratings agencies. Frankly, credit ratings agencies are usually behind the curve when it comes to updating credit ratings. I don’t think the downgrade from Fitch will impact investors’ desire for U.S Treasuries.

To test that concept, pay attention to what the 10-year U.S. Treasury yield is today (around 4.2%) and come back in a year and see what the yield might be. If inflation shows signs of continued decline, I think it could be a good probability that the 10-year U.S. Treasury yield is lower than what it is today, again, regardless of the Fitch rating downgrade. Also, as previously indicated, I don’t think U.S. Treasuries will trade much different relative to other foreign government bonds than they have traded in the past.

Bond and Yield Implications

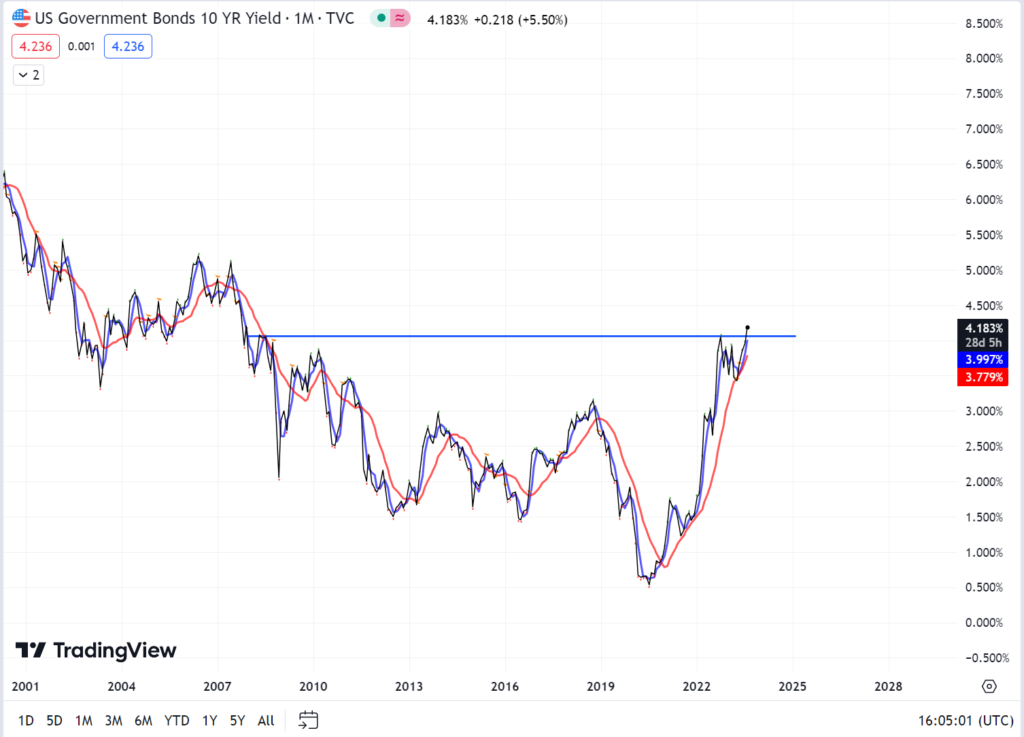

So, what’s interesting about the timing of the Fitch downgrade, is that U.S. Treasury yields have been flirting around the 4.0% mark across the yield curve. From a technical perspective (yes, technicals are tied to bonds as well, and every other asset class for that matter), the 10-year Treasury yield just jumped above the 4% level, which had been a resistance level. I would not be surprised if yields continued to move higher from here as investors that may have been short yields (believed yields would fall) need to reverse their positions and longer-term investors wait until rates spike a bit higher before coming back in and adding to bond positions.

U.S. 10-year Treasury yields are often used as an indicator for government bond yields. Not as short as the fed funds rate and not as long as the 30-year, so kind of right in the middle. As you can see in the graph below, 10-year U.S. Treasuries had hit 4% and had been bouncing around a bit. Now the next level of resistance is in the 4.5-5% level. There is a fundamental case for yields to move up, but I think the fundamental case for yields to move lower from these levels over the next couple of years is much stronger. For that reason, investors may start to consider adding to longer-term interest rate sensitive bonds at these levels. I don’t think a 4.5-5% 10-year Treasury yield, if it even gets there, stays there for long as big money comes in to lock in those yields for longer.

Source: Tradingview.com 8/3/23

Remember: As yields move higher, bond prices move lower, and vice versa. If rates continue to move higher from here over the short-term, interest rate-sensitive bond values can experience decline. As a longer-term investor, I personally wouldn’t worry too much about it and I’d prefer to start locking in higher yields for longer, anticipating yields to come down from current levels over the next couple of years.

Summary

So, in my mind, the Fitch downgrade is a bit of a non-event. It’s just Fitch telling us what we already know. If Treasury yields, and correspondingly high-quality credit yields, spike, it may be a great opportunity for longer-term investors to lock in these higher yields for longer. I don’t think they will stay high for very long.