Following the November U.S. elections, there was a general sense of investor bullishness based on what I considered a “default” belief that Republicans are good for the economy and risk assets. My concern was that even with a Republican sweep of the November elections, there was still a ton of uncertainty around inflation, tariffs, taxes, government spending and immigration.

Feel free to read my views on the elections and their impacts on the financial markets and economy here…

- Outlook & Positioning – December 11, 2024

- After the Election: Setting the Goalposts – November 19, 2024

President Trump has announced tariffs on Canada, Mexico, China, and Europe with more potential tariffs to come. As I’ve written about before, this can be inflationary on American consumers as companies push their higher import costs down to consumers. Reciprocal tariffs could potentially add even more upward pressure to prices. Higher prices can result in less spending power for business and consumers and creates uncertainty.

Another source of uncertainty has been Elon Musk and his Department of Government Efficiency (DOGE) team sending notifications to government employees that they may be terminated from their position. I don’t think such a broad sweep of potential government layoffs so soon was anticipated by most, thus probably not priced in by the markets. Regardless of any material economic impact from potential layoffs or even from the creation of short-term inefficiencies due to government confusion, this at least adds to the uncertainty.

Then add into the equation that half of voters lean Democrat and may not have wanted the election results that occurred. If President Trump and Republicans offer fiscal policies that Democrats are not happy about, that could add more uncertainty for half of the voting population. This also assumes the voters that lean Republican are confident and certain with those policies themselves. If not, well, then there is more uncertainty to add.

I also remember that Trump’s leadership in his last term was a bit chaotic, where investors (including myself) and businesses often had to try to navigate around persistent uncertainty. Anticipating uncertainty adds to more uncertainty and we are just over a month into Trump’s presidency.

With increased political uncertainty in the U.S. right now, there are enough business leaders and regular citizens that could become increasingly cautious. This can result in people being increasingly cautious, reduce spending and reduce risk taking as confidence starts to decline. I think this is what we’ve been seeing and recent economic data may be confirming that.

Sentiment and Economic Data Show Signs of Weakness

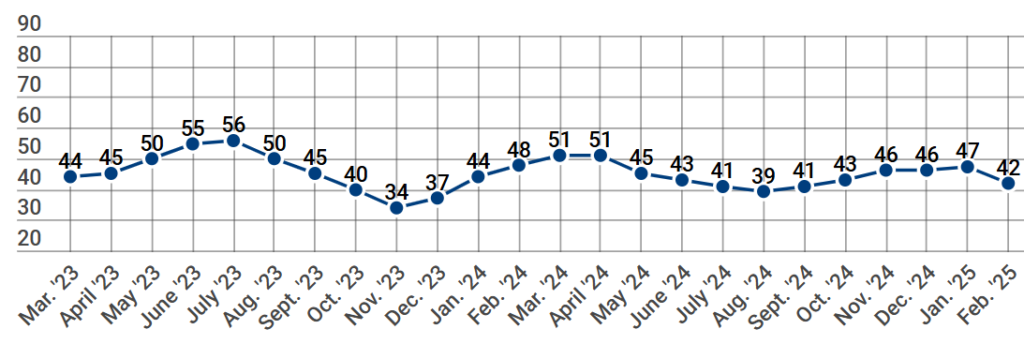

The first weaker sentiment reading that I noticed was homebuilders sentiment. In February, the National Association of Home Builders/Wells Fargo Housing Market Index declined to a 5-month low to a 42 reading. Higher interest rates, potential tariffs on lumber and deportations impacting available labor could have resulted in weaker housing sentiment.

Following the homebuilders sentiment reading, U.S. PMI numbers came out for services and manufacturing. US Composite Flash PMI Output Index declined from 52.7 in January to 50.4 in February, a 17-month low. The data showed a big drop off in services, with a bit of a tick up in manufacturing. On the services side, the largest component of our economy, suggesting that the weaker reading may indicate general business uncertainty and preparation for a slowing economy. On the manufacturing side, if manufacturers are trying to front-run tariffs, then a spike in manufacturing activity shouldn’t be surprising, and that’s what we’ve seen. If there is front-running, then there may be a giveback and weaker manufacturing PMI in the future.

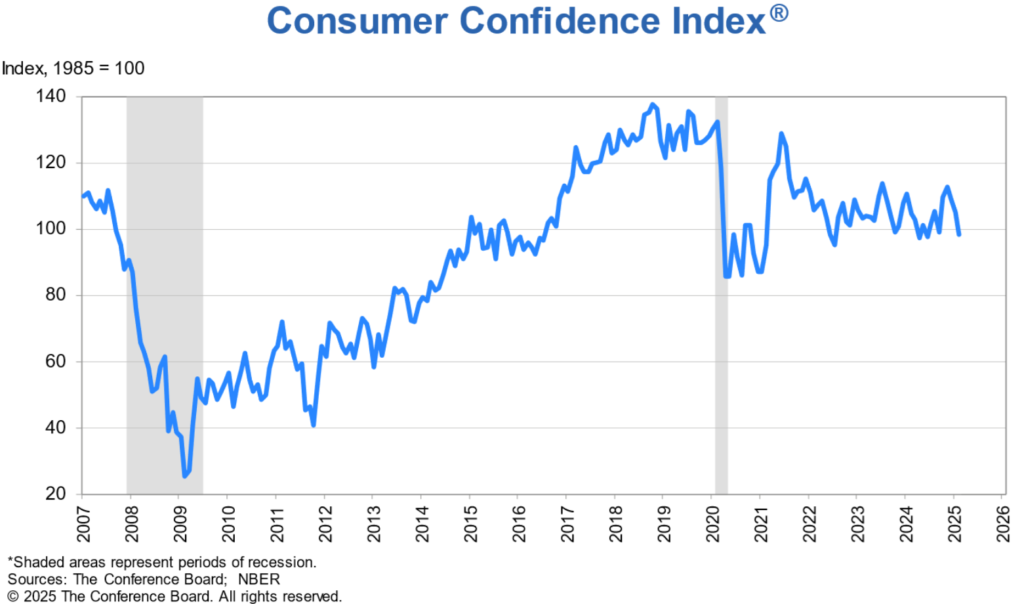

Then, the Conference Board’s Consumer Confidence Index for February declined to 98.3, marking the largest drop since August 2021. Lower consumer confidence can lead to lower consumer spending and a weaker economy.

So as we sit here today, a lot of the political uncertainty in the U.S. may now be starting to impact business and consumer sentiment, which may ultimately impact spending and then corporate profits. I think the market has started to pick up on this, resulting in equities and other risk assets selling off and bonds and other safe assets rallying.

Market Technicals Weakening

I’ve written about high valuations in U.S. equity markets for a while, so just from a non-technical, fundamental perspective, high valuations in U.S. large caps just aren’t that attractive from a short-term perspective. Over the short-term, valuations alone don’t often move markets, but market technicals do. Let’s take a quick look.

I’ve been keeping an eye on small caps for a while. I indicated the resistance level in small caps in my December Outlook & Positioning article, which they couldn’t overcome. Now I see small caps breaking below the 200-day moving average (red line), with potential bearish pressure from a declining 50-day moving average (blue line). This downside pressure could help to get small caps to my buy target, so I’ve been watching this very closely.

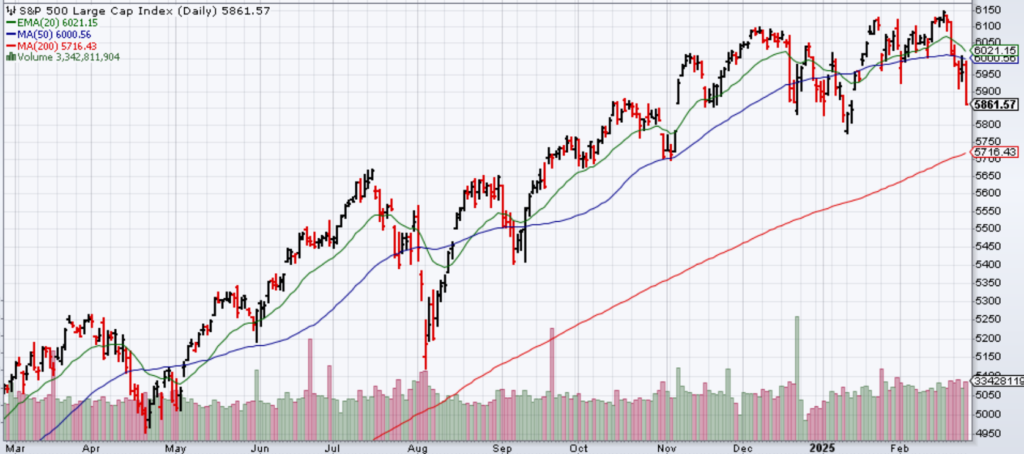

The S&P 500 still has some ways to go until it hits the 200-day MA, but even with the recent decline, we haven’t broken below the lows we hit in January, so maybe not as bad as people might think the recent decline has been.

The technology-heavy NASDAQ 100 index has been weaker than the S&P 500 Index due to significant declines in some of the large technology companies in the NASDAQ. Tesla’s stock has been experiencing significant weakness, potentially due to the actions of Elon Musk and his government work with DOGE negatively impacting the Tesla brand. Nvidia’s stock has also weakened, as questions arise about how much sophisticated chip infrastructure is truly needed to run AI models and what the tangible payoff of AI will be, given the heavy upfront investment cost.

If equity markets continue to experience weakness, this can start to make more investors nervous and result in further selling pressure. Just remember, technical setups don’t always have to follow through. Some positive or negative fundamental news could impact market technicals and trends could be reversed. This is why I don’t necessarily trade on technical trends, but I am aware of how they can impact the markets.

So What Am I Doing From an Investment Perspective?

If you have been reading my other commentaries, you should know I have been patiently waiting for the market to come to me. U.S. equity markets are now starting to turn towards me and getting closer to getting interesting again.

I generally need markets to decline enough for me to consider adding risk. I like to add risk after a selloff and reduce risk after a rally. I like to keep it simple.

As it stands right now, U.S. large caps aren’t interesting enough, mid caps are sort of interesting but small caps are almost juuuuuuussssssttttt right. If small caps keep declining a bit more and reach my price target, I’ll increase my exposure to small caps in what I would call an initial tranche. If they don’t hit my price target, I’ll just rebalance (top off exposure) where it makes sense to do so. If large and mid caps get to my target levels, I’ll do the same there.

I also have some tactical positions that I’m watching. I recently rebalanced (took some profits) in Chinese equities that rallied back to my high target. Positions in semiconductors, small cap biotech and broader emerging markets have some ways to go for me to increase risk exposure, but if they hit my target, I’ll be adding to those areas again.

From a multi-asset income perspective, I need pure equity exposure to decline much further to consider reducing exposure to lower volatility multi-asset income strategies to increase pure equity exposure.

Within fixed income, interest rates across the yield curve had jumped higher in January, with the 10-year Treasury yield close to 4.80% for a bit and the 30-year Treasury yield close to 5%. I had said in previous commentary that I would be more bullish on bonds and taking interest rate risk if the yield curve was above 4.5%, and that was indeed the case. Now, as economic data has shown some weakness, bonds have rallied and the yield curve has quickly fallen from their highs. The 10-year Treasury is now below 4.3%. If the 10-year Treasury yield continues to decline below 4% and approaches 3.5%, I would become more bearish on interest-rate-sensitive bonds.

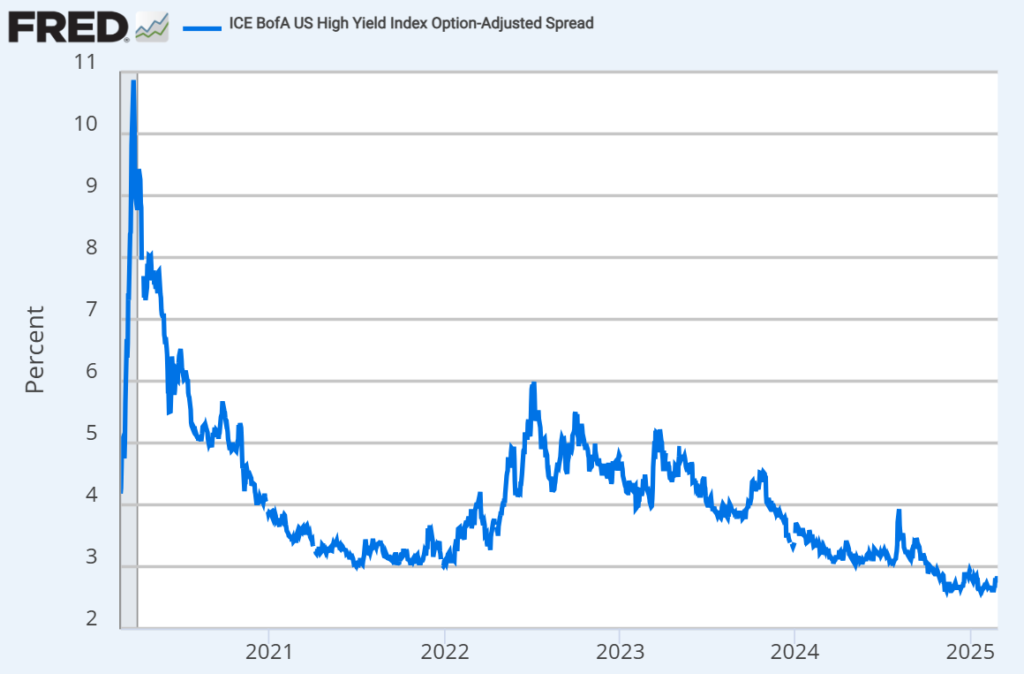

From a credit risk perspective, credit spreads are still way too tight, so I don’t anticipate adding any significant credit risk to my conservative bond allocations. I would need to see credit spreads widen significantly from here to do so.

Summary

I think investors may start to get impatient if strategies around key fiscal issues around inflation, tariffs, taxes, government spending (and cuts to get there) and immigration aren’t clarified or resolved. Recent economic data indicates that businesses and consumers may be becoming less confident, which can directly transfer through to the U.S. economy. investors will need to wait to see if recent data is just an anomaly or if this is the start of a broader, more persistent trend.

In periods of uncertainty, markets will often sell first and ask questions later, so it remains to be seen how financial markets will continue to react. For me, as always, I’m just waiting for that fat pitch down the middle and I’ll be ready to swing.