SUMMARY

Volatility finally picked up in the equity markets over the last couple of months. Patient investors waiting for a better opportunity and looking to add risk may have been rewarded if they “bought the dip”.

In August we finally had the correction in artificial intelligence-related stocks, which I had been waiting for. Prior to August, valuations appeared stretched at the time and investors continued to be giddy on the prospects of AI. Until they didn’t.

From the peak in July to the bottom in August, the Philadelphia Semiconductor Index fell over 30%, the NASDAQ 100 index dropped more than 15%. As I had been patiently waiting for an opportunity, I bought the dip in leveraged semiconductors and leveraged NASDAQ 100 ETFs across my tactical strategies. From there, these areas rallied quickly and I essentially cut those positions in half and am holding the rest until they hit my higher price targets. I don’t tactically trade a lot, but when there is what I believe to be a fat pitch down the middle, I’ll swing.

Source: StockCharts.com 9/16/24

Elsewhere, equities continue to catch a bid, particularly in some of the non-technology and non-“Magnificent 7” areas of the market. Investors that had been diversified across sectors, market cap and geography were rewarded in the last few months. Again, I prefer diversification, so this has been beneficial to my positioning. I’ve maintained this diversified positioning and don’t anticipate changing it any time soon. I maintain leveraged exposure across U.S. market caps, emerging markets and some dedicated leveraged positions in semiconductors, U.S. biotechs and Chinese equities.

Fed Rate Cuts

On Wednesday, September 18th, the U.S. Federal Reserve cut the fed funds rate 50 basis points (0.50%) to a target of 4.75%-5.00%. There was a lot of speculation and what seemed to be a lot of hand wringing whether the cut would be 25 or 50 basis points. I don’t really care about the first rate cuts, which have been largely anticipated. I care much more about where the cuts might end and whether the economy can just moderately decelerate and hit that soft landing. If we can get to that steady, slow-to-moderate growth rate, without a significant economic decline, risk assets could continue to be supported by investors.

November Elections

We have the presidential and congressional elections coming up in November. The election results in and of itself aren’t overly worrisome to me, the policies that are enacted from whoever is in office is key. The biggest policies that I’m paying attention to are around the expiration of the lower tax rates at the end of 2025.

If whoever is in political power can navigate the tax expirations without significant changes (I think taxes will be higher), then even some tax increases may not be that detrimental to the economy and corporate profits. I think U.S. citizens and companies will adjust as they always do. Interest rates jumped from essentially 0% to over 5% and it appears people were able to navigate it just fine. People and companies adjust.

As an investor, I focus on policies and try not to get emotionally driven by the rhetoric of each political party. I think it’s a mistake to overly speculate on investment outcomes based on election outcomes. Adjusting one’s investments shortly after the elections based on their political views may not result in the investment outcomes that they thought would occur. Again, try not to let emotions drive your investment decisions.

People that trade their investments based on political speculation often forget that the fundamentals of their investments may not change all that much regardless of which political party is in power. Equity investors are invested in companies with management teams that are trying to generate profits regardless of political party. Bond investors are invested in bonds that are often structured to pay income and pay back principal to their investors, regardless of political party.

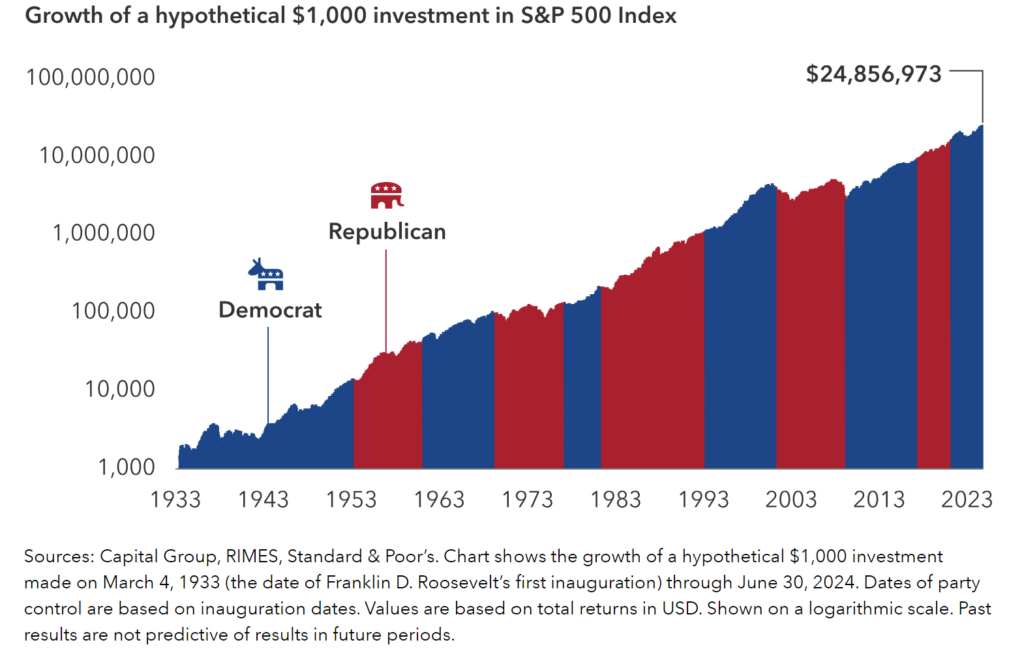

Take a look at the long-term chart below of the S&P 500 Index overlayed with the different periods of Democratic/Republican presidents. Investors that closed their eyes and invested in the S&P 500, even if they didn’t believe in the policies of the political party in power, would have been rewarded over time.

RISK ASSETS

As a long-term investor, I have my long-term diversified allocation across risk assets with some leveraged positions in areas that I believe have both short- and longer-term potential growth. I’ll continue to rebalance and try to take advantage of volatility whenever it makes sense for me to do so.

I’m still slightly bullish on risk assets, anticipating volatility to continue. Valuations in U.S. technology-related large cap companies continue to appear a bit extended. Valuations in other areas across market cap, sector and geography seem more palatable, but they’re not “pound the table” cheap.

I continue to like high quality growing companies and am mindful of valuations. As a long-term investor I know I’ll need to hold through periods of higher valuations (like today’s environment) and that trying to time markets based on valuations is tough to do, so I don’t do it.

There does appear to be some potential opportunities in deeper value cyclical stocks where performance has lagged. If the Fed continues to cut rates and the economy can decelerate without a ton of issues, these lower valuation cyclical stocks could catch the attention of investors. To capture this more cyclical exposure in my investments, I’m allocated to U.S. and global deeper value active equity managers that have a bit of a cyclical tilt. I’d rather have these equity managers find the deeper value opportunities than try to use some sort of passive value strategy agnostic to fundamentals.

I continue to like multi-asset income strategies, so if we’re in more of a choppy investment and economic environment, I’m at least generating attractive income from a portion of my investments. Exposure across option income, high yield corporates, dividend growth and closed end funds remains a nice income generator for me.

U.S. EQUITIES

When the U.S. equity market trades at a premium relative to history, the market may be subject to a downside correction. Another path for the market could be to just chop around until earnings growth catches up to price. No one knows which path the market will take, but it could mean at least future returns over the next few years may be below average.

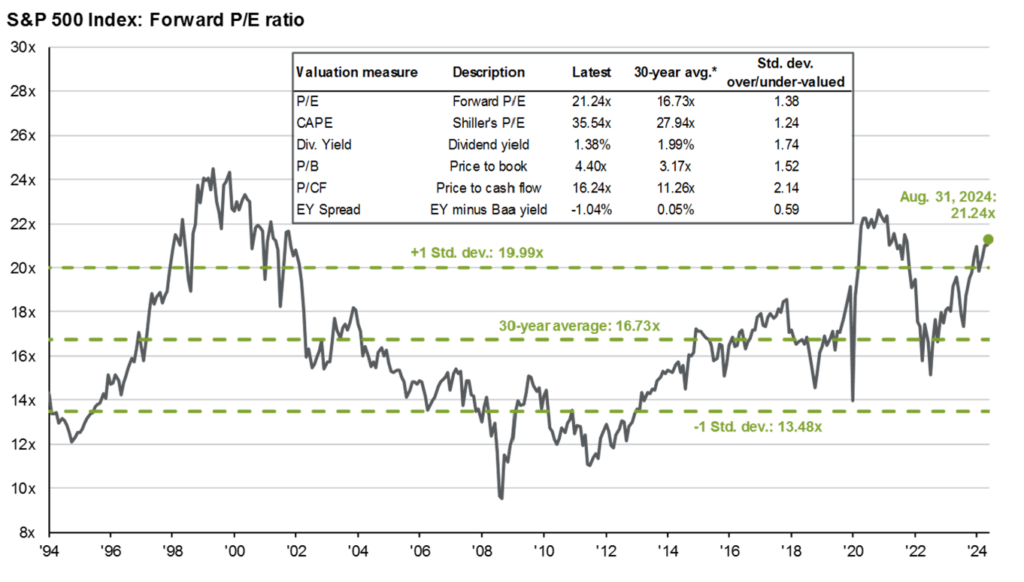

At least looking at the valuations graph and metrics below, the S&P 500 Index doesn’t look cheap. While valuations aren’t a great timing tool, I continue to be slightly bullish on U.S. equities.

Source: JPMorgan Guide to the Markets, August 31, 2024

Outside of the S&P 500 Index or broad U.S. large cap indices, I continue to prefer exposure and diversification across mid and smaller cap stocks to complement my large cap exposure. Across market caps, I continue to prefer to focus on higher quality, growing companies across sectors. These areas have rallied a bit more recently, which is good, but time will tell how persistent that strength will be.

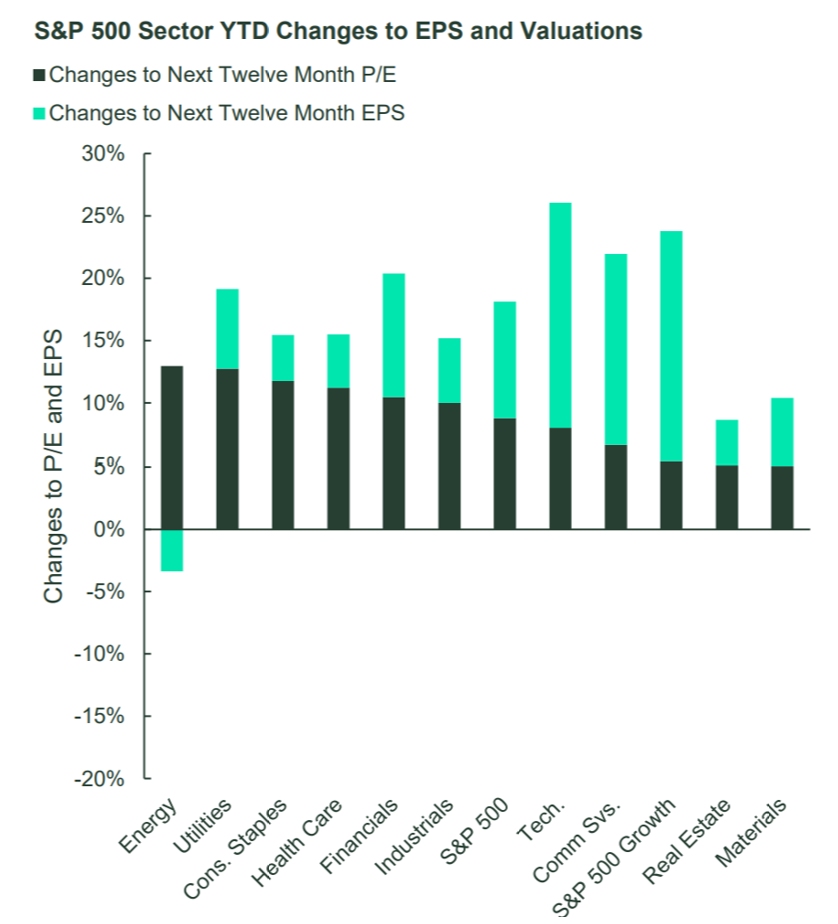

Interestingly, what some investors would consider “defensive” sectors of the market, including utilities and consumer staples, have experienced a pretty significant rally. Following the rally, current valuations in these areas have become a bit too stretched for me in the short term. So if tech-related and now defensive areas’ valuations are becoming elevated, it appears that valuation risk is heightened more broadly across the market.

Investors should be reminded that defensive areas of the market can get to valuations that may not be overly attractive. In the chart below, you can see the forward P/E ratio (black bar) for utilities, staples and health care (often considered defensive sectors) has jumped higher, indicating valuations have increased. At this point for me, these defensive sectors don’t seem that attractive over the short-term and I’d personally be cautious, especially for investors that believe these sectors are “defensive”.

Source: State Street Global Advisors. SPDR® ETFs Chart Pack. September 2024 Edition

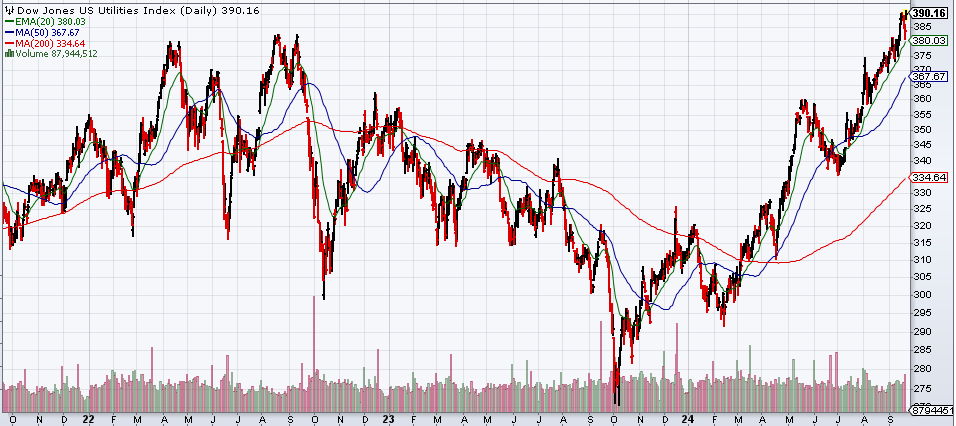

You can also see the technical chart of the Dow Jones U.S. Utilities Index (below) rallying significantly from its October 2023 bottom. In my opinion, these so called “defensive” sectors, shouldn’t really be considered defensive. Look at the decline from October 2022 to October 2023 in “defensive” utilities, where investors were down roughly 30%. Not what I would call “defensive”.

Source: Stockcharts.com 9/20/24

Markets have changed over the years and are much more volatile. Using a particular equity sector (utilities) as a defensive asset class may not always actually be defensive as hoped. Just remember, equities are volatile and they are not defensive or conservative investments over short periods of time, regardless of the sector they are in.

FOREIGN EQUITIES

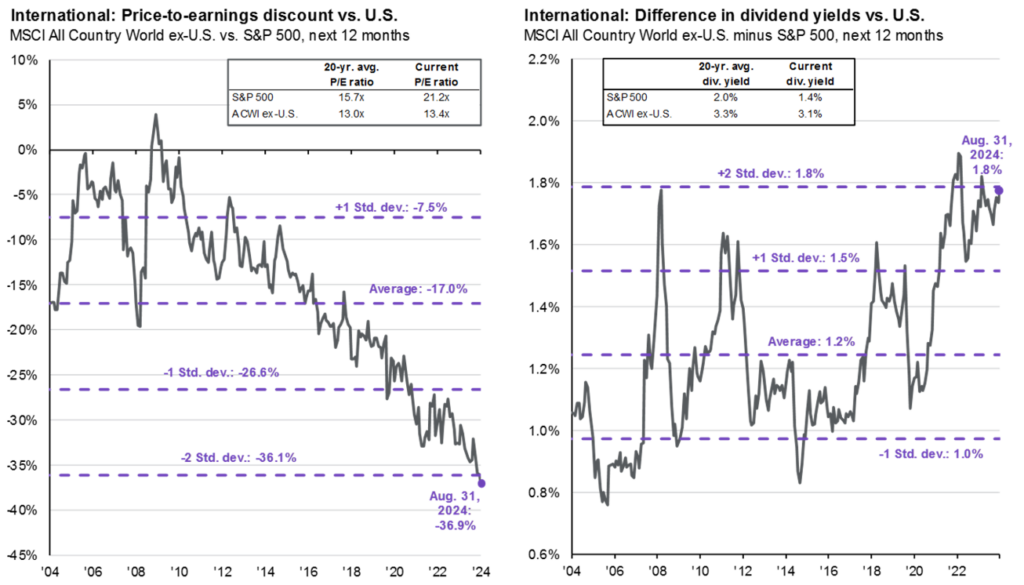

I continue to believe there are strong, high quality, growing companies throughout the world. While the U.S. is my preferable place to invest from a market security and regulatory oversight perspective, the valuation discount in international markets remains attractive, in my opinion. I continue to remain moderately bullish on foreign equities at this time.

The graphs below show the valuation of international equities’ price-to-earnings ratios and the difference in dividend yields versus the U.S. While I don’t want to dig that deep into the analysis in this commentary, these are just two data points to look at when determining short-term relative valuations between U.S. and international equity markets. Just consider it a starting point.

Source: JPMorgan Guide to the Markets, August 31, 2024

HIGH INCOME

It’s tough for me not to be continuously moderately bullish on diversified high income asset classes. High yield bonds continue to generate yields at 7%+, option income strategies can generate yields of 6%+, I can get diversified exposure to closed end funds and generate yields of 8%+ through that exposure, and diversified credit-sensitive bonds can hit yields of 5%+. If my estimate of longer-term diversified equity returns of 7-8% is correct, diversifying to higher income generating assets with attractive returns from yield generation makes sense to me.

Equity markets have rallied strongly in the U.S., we’re close to new highs and valuations aren’t cheap from my perspective. For me, it makes sense to have diversified exposure to higher income-generating assets to potentially provide some downside protection relative to equities, generating income in flat equity markets, and be a source of “drier powder” to allocate to equities if valuations become more attractive at some point.

COMMODITIES

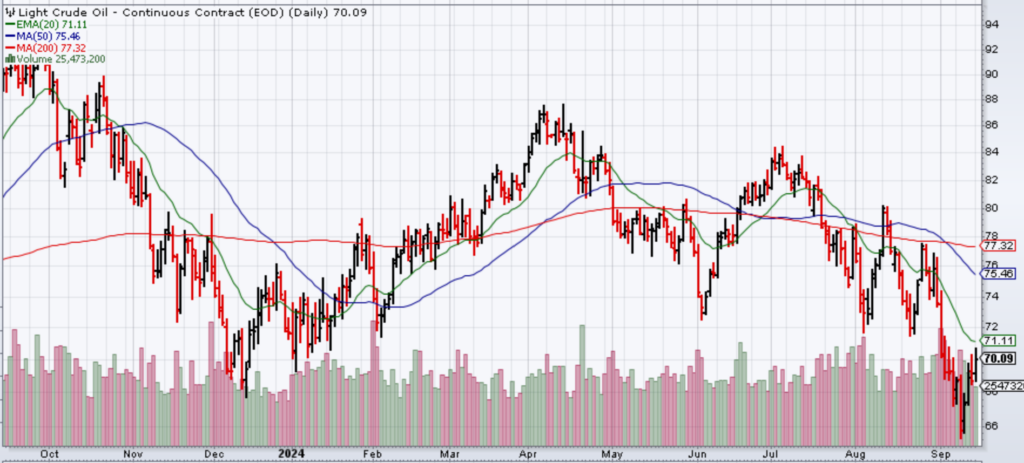

In my last Outlook and Positioning commentary that I published in June, I turned slightly bearish on commodities as I thought investors would start to price in a continued slowdown in the U.S. and China’s economy just couldn’t get going. As inflation continued to slow and the economy decelerates, commodity prices continued to trend downward.

WTI Crude Oil, which I think can trade between $60-$100 on average, which is a wide range, declined to around $65 per barrel in September. At those lower levels, I couldn’t be as bearish as I was so I turned slightly bullish at that time.

Source: StockCharts.com 9/16/24

Copper prices also continued to decline the last few months, so I can’t be as bearish as I was on industrial metals in general. Copper and other industrial metals may get a pickup in investor interest over the longer-term. The long-term need for traditional and new technology infrastructure could require increased demand for copper and other industrial metals, so I prefer to be a bit more bullish on industrial metals following the selloff through early August.

Source: StockCharts.com 9/16/24

It remains to be seen whether the global economy can gradually decelerate without a significant slowdown or recession. Even if the economy hits a rougher patch than anticipated, and even if commodities take a leg lower, I think at some point commodities can catch a bid and move higher than current levels based on the long-term needs for commodities.

As mentioned many times, I’m not a fan of gold as the reasons to own gold seem to change all the time. Although gold has continued to attract investors and push the price higher, I’m won’t have a dedicated allocation to gold, silver or any other traditional precious metal.

CONSERVATIVE ASSETS

Interest rates across the yield curve have declined from their highs and bond prices rallied over the last couple of months. In the Outlook and Positioning commentary I published in June, interest rates across the yield curve were above 4% at the time. That level of yields still seemed attractive to me at that time. That’s no longer the case as yields have declined across the yield curve. Following this rally in bonds, I’ve changed my view on conservative assets from moderately bullish to slightly bullish.

From a bond perspective, intermediate- and longer-term bonds have already rallied a bunch, so being overly long duration may not make sense any more. I would prefer to be fairly neutral duration relative to an intermediate-term bond index at this point.

Interest rates across the yield curve could continue to grind lower over the short term as the Fed cuts the fed funds rate. From a longer-term investment perspective, with a heavy U.S. debt burden, intermediate- and longer-term interest rates may not fall materially lower from current levels. If bond investors believe that U.S. credit worthiness is less worthy, credit risk might also need to be priced in, resulting in structurally higher longer-term interest rates.

At this point, I would rather be allocated to the intermediate part of the yield curve, without a ton of duration exposure on the long end and with less reinvestment risk on the very short end of the curve. If the yield curve continues to shift lower from here, I’d probably start to reduce duration as the long-term U.S. debt level may force interest rates higher over time relative to current levels. Remember, for interest rate-sensitive bonds, as interest rates fall, bond prices can increase. If interest rates rise, bond prices can decline.

Within fixed income, I prefer to allocate to active bond managers that can allocate across sectors, manage duration, tactically allocate across credit qualities and provide exposures I can’t get directly. Structurally, for me, allocating to a passive bond strategy just doesn’t make any sense.

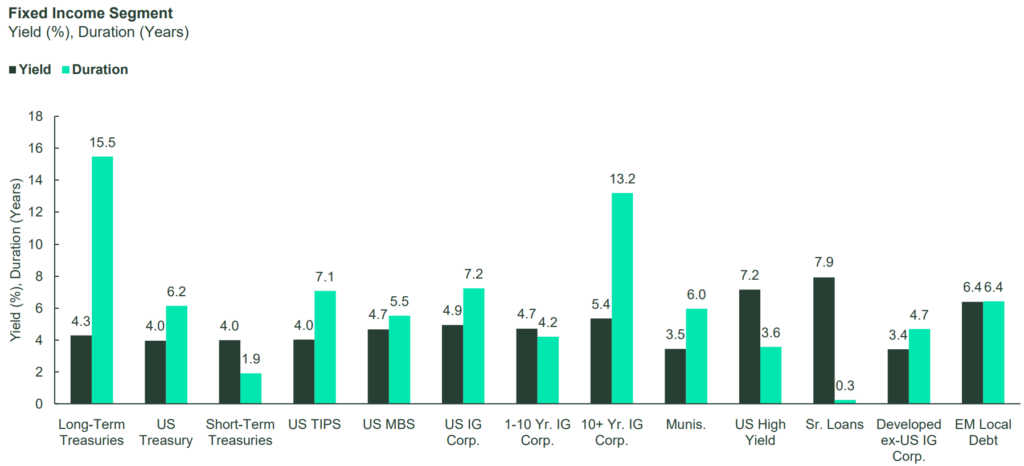

As you can see from the chart below, these are just some of the bond sectors and maturity profiles with current yields and duration (interest rate risk) exposure. Again, for me, I’m allocating to active bond managers to navigate the bond market rather than attempting to make tactical adjustments across the complex bond universe.

Source: State Street Global Advisors. SPDR® ETFs Chart Pack. September 2024 Edition

U.S. GOVERNMENT BONDS

If I have to own bonds, I’m not having a ton of exposure to government bonds. I would rather take additional credit risk and accept higher potential volatility for higher potential returns by investing outside of U.S. Treasuries and agency bonds.

For conservative investors, from an absolute yield perspective, the yield curve is still above 3.5% across most maturities, but is down from 4%, when it was more attractive. With yields shifting lower across the yield curve, for me, government bonds are just less attractive from a long-term total return potential perspective. So in order for higher potential returns, you may need to accept higher volatility in credit-sensitive bonds. As someone who can handle the added volatility, I’m more bullish on credit-sensitive bonds than I am on U.S. government bonds.

U.S. INVESTMENT GRADE CREDIT

Knowing the vast opportunity set across investment grade credit-sensitive bonds, I’ll always maintain a preference for credit-sensitive bonds over government bonds. I’m willing to take on that added potential volatility for that added potential total return.

I prefer to remain allocated to investment grade bonds across sectors credit, loans, securitized/mortgages, etc. and across the intermediate part of the yield curve. I am willing to have some high yield / below investment grade exposure through my active bond manager allocations, but I’m not overly allocating risk here, I’m just remaining fairly neutral at this time.

OTHER

I use this section to talk about other potential strategies, generally whether or not hedges are needed on asset classes.

Prior to the correction in artificial intelligence-related stocks, some sort of equity hedge or allocation to non-technology or income-generating assets made sense. After the selloff in tech, that hedge made less sense as a 15-30%+ selloff provided opportunities to take off that hedge and buy the dip, which I did.

Now that the markets have rallied again, maybe some sort of risk reduction (equity hedge, lower volatility options, income generation, etc.) makes sense again. For this reason, at this time, I’m remaining slightly bullish on hedging some equity exposure in the more tech-sensitive and “defensive” sectors (utilities, etc.) of the market that have quickly rallied significantly from the August selloff.

I didn’t feel any real need to have a hedge on bonds, and even with interest rates below 4% across the intermediate- and longer part of the yield curve, I’m more neutral on bonds. If I had a hedge on bonds it would probably be more on the long end of the curve where duration risk is high and longer-term bond yields could move higher from current levels.

Credit spreads are still relatively tight, but there doesn’t seem to be a ton of pressures in the credit markets. With interest rates coming down, there may be less credit pressure for bond issuers than there was under a higher interest rate regime. So from a credit perspective, I don’t feel much of a need to hedge credit exposure at this time.