SUMMARY

Remember volatility? Here we are again.

Following the Republican sweep in the November elections, investors were optimistic about the potential for a strong business environment under Republican leadership. I’m not going to rehash my commentary on and concerns with the potential issues surrounding tariffs, government spending cuts, immigration/deportation, inflation pressures, etc., but these are the factors that appear to have come to the forefront of investors’ minds.

Based on my previous commentary, in summary, I didn’t want investors to just believe by default, that Republican political leadership automatically means a great economy and equity markets will rally. Things are a lot more nuanced than that and that’s what I think investors are starting to question as political uncertainty persists.

You can read my past views on the election and things to keep an eye on here:

- Political Uncertainty and Weaker Economic Data Impacting Financial Markets February 27, 2025

- Market Update Q4 2024 January 6, 2025

- After the Election: Setting the Goalposts November 19, 2024

- Don’t Let the Emotions of Politics Impact Your Investment Decisions November 16, 2024

So here we are. Equity markets in the U.S. have quickly declined from their recent highs. Investor sentiment has declined. Economic data has been weaker. U.S. government leadership continues to create headlines around tariffs and government spending cuts. Sure feels at least less bullish to me.

This is why I continue to focus on letting the markets come to me and not me trying to overly speculate what the markets will do based on various factors. This is based on many years of watching investors making mistakes by often buying and selling at the wrong time for the wrong reasons.

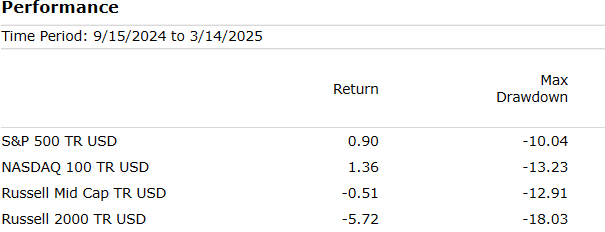

In any given year, equity markets can decline 10-15%, sometimes more, sometimes less. Let’s get an update on the total peak to trough (maximum drawdown) for a few U.S. market indices and compare it with their total return over the last 6 months…

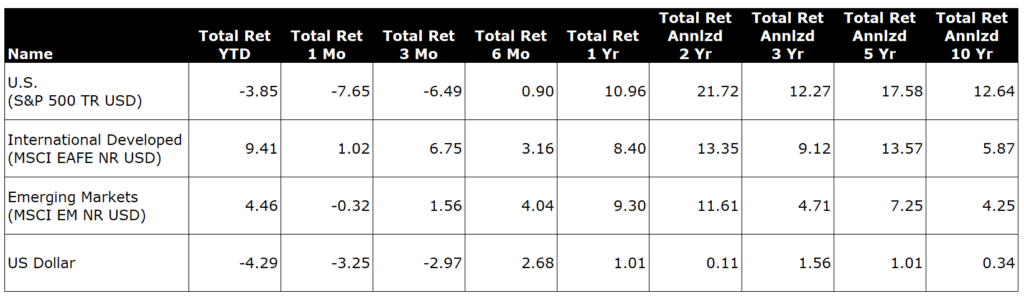

Looking at the table above, the S&P 500 is down 10% and the NASDAQ 100 is within that 10-15% selloff range. Mid caps and small caps (Russell 2000) are right around that range as well. Taking a 6-month view going back to September, diversified investors are just fine, and could still be ahead depending on how they were allocated.

Although parts of the U.S. equity market have sold off, credit spreads have only slightly widened and international equities have rallied. While there is uncertainty, it might take a lot more uncertainty to flow through a relatively durable U.S. economy.

Remember, markets don’t have to crash. Equity markets consist of companies, with management teams that need to adjust and navigate whatever political environment we’re in. If we continue to lack clarity on fiscal policy, equity and bond markets might just remain volatile but not decline materially from here since we’ve already had a bit of a correction.

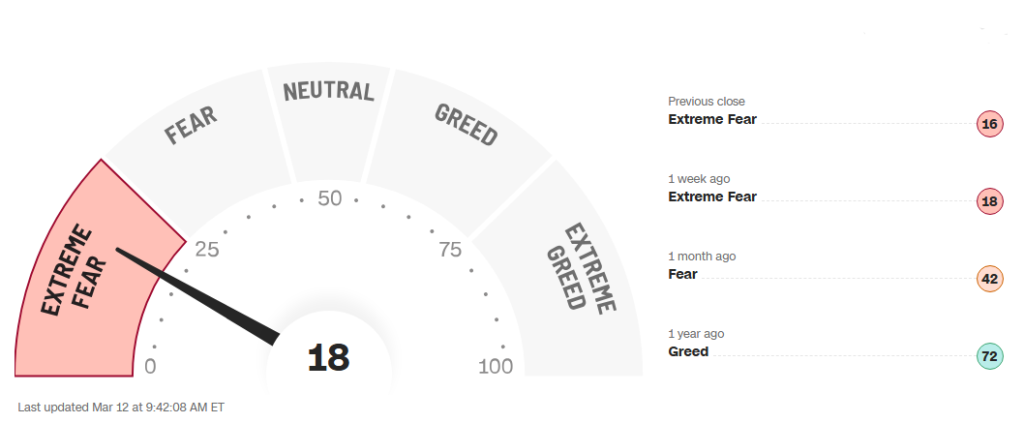

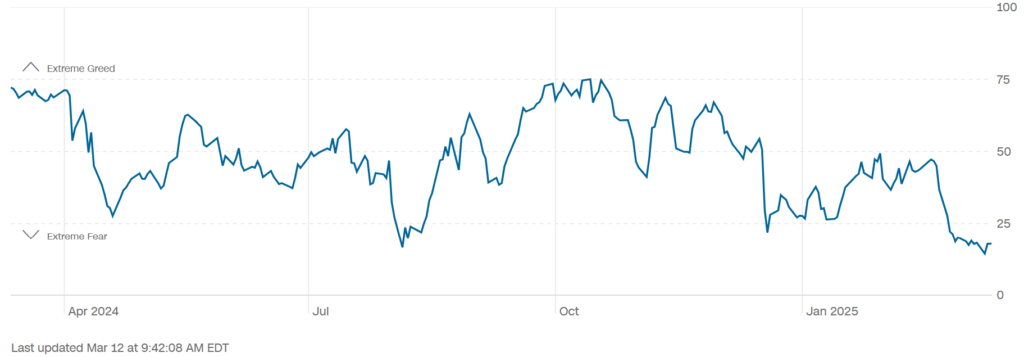

If we take a look at investor sentiment, defined by the CNN Fear and Greed Index shown below, it’s at the lower end of the range, indicating, at least quantitatively, investors have been selling and may be bearish. Based on the various headlines, discussions and overall vibe I’m getting from various investors, it seems like some have already reduced risks in their portfolios. From my perspective, this is capital these investors may need to put to work again and could push the markets higher over time.

CNN Fear and Greed Index

Is this a pound the table, buy everything market? Nope, but one might consider at least knocking the table a bit and adding some risk if they’ve been neutral or underweight risk, like I’ve been doing. From my perspective, I’m just sticking to my process, letting the market come to me and will increase exposure to risk assets if the markets decline further from here.

If other short-term tactical investors are bearish, as a longer-term investor, I’m not afraid to take the other side. In this situation, this is the kind of pitch I want to swing at.

What Am I Doing in this Environment?

So what am I doing? I’ve been sitting in the batter’s box since October/November at my neutral risk position and lowest allocation to tactical leveraged positions. I’ve just been waiting for a decent pitch. Now, following the U.S. equity market decline from its highs, I started swinging the investment bat. I’m looking for that single. Not a double, not a home run. Just a single.

Don’t know what I’m talking about? Feel free to read my article on swinging at the fat pitches here.

Investing: Swinging at the Fast Pitches Down the Middle October 4, 2024

What have I been doing specifically? I started to tactically increase exposure to small/mid caps and the NASDAQ, with additional tactical rebalancing (buying lower) in select positions.

I have no idea where the market will go from here. I don’t know if the political, economic, investment environment gets better or worse from here. What I do know, is that by focusing on the long-term, staying diversified, allocating to higher quality growing companies around the world, allocating to higher income-generating assets and not taking on a ton of unnecessary risk at this point, I’ll be fine.

If risk assets continue to decline from here, I’ll continue to add risk exposure. If bond yields move higher, I’ll become more bullish on bonds. I’m just focused on hitting singles right now and if the markets give me those fat pitches down the middle, I’ll be swinging harder for those extra bases. We’re just not there yet from my perspective.

Remember, financial markets don’t care about anyone’s political beliefs, so don’t let your beliefs impact your investment decisions. Over the longer-term, fundamentals win out. The markets will let us know whether fiscal policies implemented today might be good or bad. Financial markets will ultimately be driven by the economic and corporate data that results from those policies.

This is me “cutting through the noise”. This uncertain environment is just another reason why I’m a patient, long-term, diversified investor that lets the market come to me rather than speculating on political decisions or any other particular factors.

RISK ASSETS

Although U.S. equity markets have declined, international equity markets have actually rallied. Higher income-generating assets have also either declined less or have actually rallied in this environment, depending on the asset class. In this environment, I still remain only slightly bullish. If we get a deeper decline across all risk assets, I might change my view from slightly bullish to moderately bullish at that time. I’m nowhere close to that point across all risk assets yet.

Even after the U.S. equity market decline and rally in foreign equities, U.S. equities still trade at a material premium to foreign equities. I continue to remain diversified with exposure to foreign developed and emerging market equities. The Trump administration’s drive towards higher tariffs is an issue, particularly with what appears to be a lack of backing down from foreign countries, at least for the time being.

If there is a renewed sense of nationalism and weaker perception of the U.S. by foreign countries’ governments and citizens, those foreign countries may embark on increased spending and economic support for their own domestic purposes. This could result in less support for U.S. markets and more support for non-U.S. markets by investors. Regardless of what President Trump’s tariff policies might be, diversification in high-quality, growing companies throughout the world continues to make sense to me.

I continue to like higher income-generating assets, which offer diversification and income support. This can be helpful in a flat or down equity market environment. These assets may also be considered “defensive” in nature (whether they actually are or not are another subject), but with higher starting yields in credit-sensitive assets, there may be a bit of a cushion on the downside, which is good. These assets can act as my “drier powder” during a broader equity market decline.

U.S. EQUITIES

Even though the U.S. equity market has declined from its highs, I remain only slightly bullish on U.S. equities. I’d like to see the S&P 500 Index decline further in order for me to get more bullish on U.S. equity markets. My default expectation for U.S. equities in any given year is a decline of 10-15%. I would need a deeper decline in the S&P 500 Index specifically to consider becoming more bullish on U.S. equities than I already am.

With that said, I did become incrementally bullish on U.S. small caps, mid caps and the NASDAQ 100 Index following the selloff in these areas. While this is nuanced, this is a tactical increase in leveraged positions as these areas declined to my target buy levels based on the tactical strategies I manage. I also maintain small leveraged allocations to semiconductors and small cap biotech that I can tactically rebalance as volatility remains elevated.

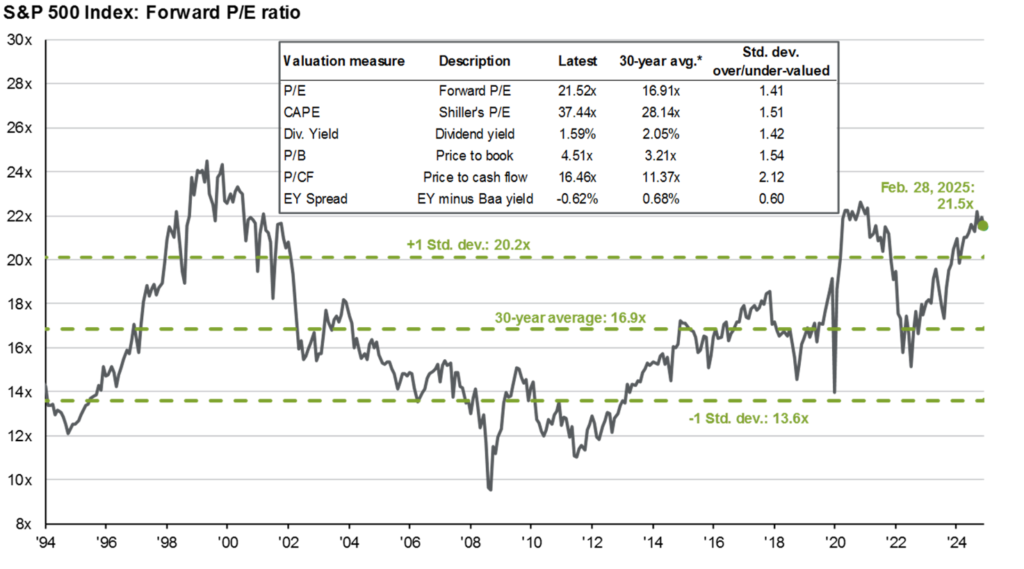

Valuations in U.S. large caps, particularly the larger technology-related mega cap stocks, remain a bit stretched, but they have come down from their highs. Valuations across mid and small caps remain favorable and I continue to allocate here from both a short-term tactical and longer-term strategic perspective.

Political uncertainty in the U.S. is at the forefront of businesses’, consumers’ and investors’ minds. The Trump administration is early in its leadership days, and a lot of uncertainty around tariffs, government spending cuts, agency changes, geopolitical relations, immigration and final tax policy remains. We have seen some business, consumer and investor sentiment surveys showing concern, but we really haven’t seen economic data deteriorate in any meaningful way, but it is still too early.

Negative sentiment can translate to weaker economic data, but financial markets attempt to front-run that data. In my opinion, this is why we are seeing weakness in the U.S. equity market before any weaker economic data is realized. Just remember, when the economic data is the weakest, it often becomes “old news”. Instead, investors then look toward a potential better economic future and equity markets start to rally higher before the improvement in economic data actually occurs.

Market Technical Analysis

From a market technicals perspective, short-term technicals have been bearish across U.S. equity indices for a couple of weeks, but there is some longer-term technical support below.

The S&P 500 Index has enjoyed very strong positive technical support the last couple of years. Only now is it showing some increased weakness, falling below its 200-day moving average (red line), often considered a potentially bearish technical signal…

When looking at the weekly technicals, there remains strong technical support below, with rising 100- and 200-week moving averages. It would take a further decline of roughly 10% and 20%, respectively, to get to those lower levels. At those levels, the total decline to the 200-week moving average would be around 25%. Just a reminder, in 2022, the S&P 500 Index declined around 28% from peak to trough, then rallied from there. If we start hitting those lower levels, my process would lead me to increase exposure to U.S. equities at that time.

It’s a similar story for the growth-heavy NASDAQ as well, but the NASDAQ has had a steeper decline…

Same on the weekly chart…

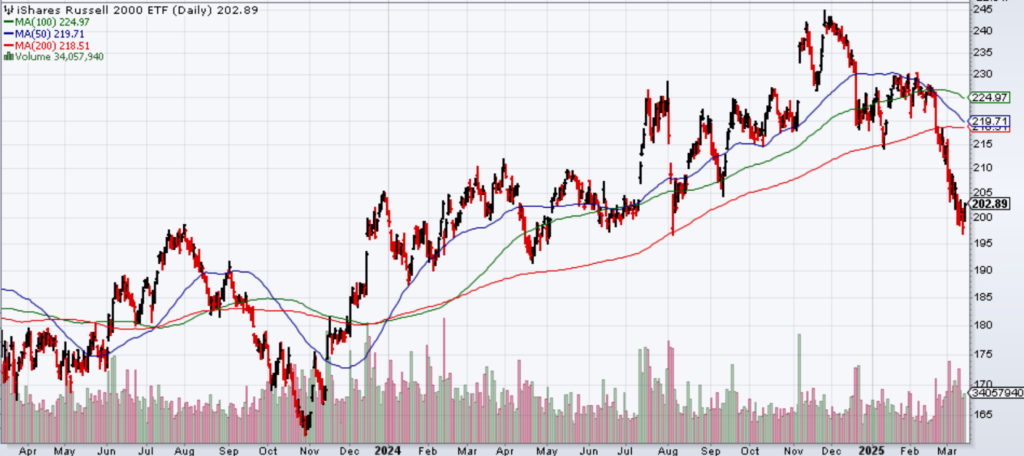

On the smaller end of U.S. equity market cap, small caps (using a Russell 2000 small cap ETF as a proxy for illustration), blew through the 200-day moving average to the downside…

…but there may be some support below when looking at the 100- and 200-week moving averages. If small caps trade below these moving averages in any sustainable basis, volatility could pick up even further and small caps could remain choppy for some time. Time will tell whether we bounce from here or continue to push lower.

Bottom Line: I have incrementally increased my risk exposure to U.S. equity markets in select areas, but will be patient to allow U.S. equities to decline further to consider adding additional risk exposure. If equities don’t decline further from here, I’m content with my current positioning.

FOREIGN EQUITIES

I continue to have a moderately bullish view on foreign equities at this time.

Foreign equities have been outperforming U.S. equities over the last few months. This has been a combination of foreign equities rallying themselves, plus the U.S. dollar has been experiencing weakness. The rally both foreign stocks and their foreign currencies have had has been beneficial for U.S. investors allocated to foreign equities. At least over the most recent term, diversification across geography has been beneficial for investors. It remains to be seen whether that can persist over the longer-term.

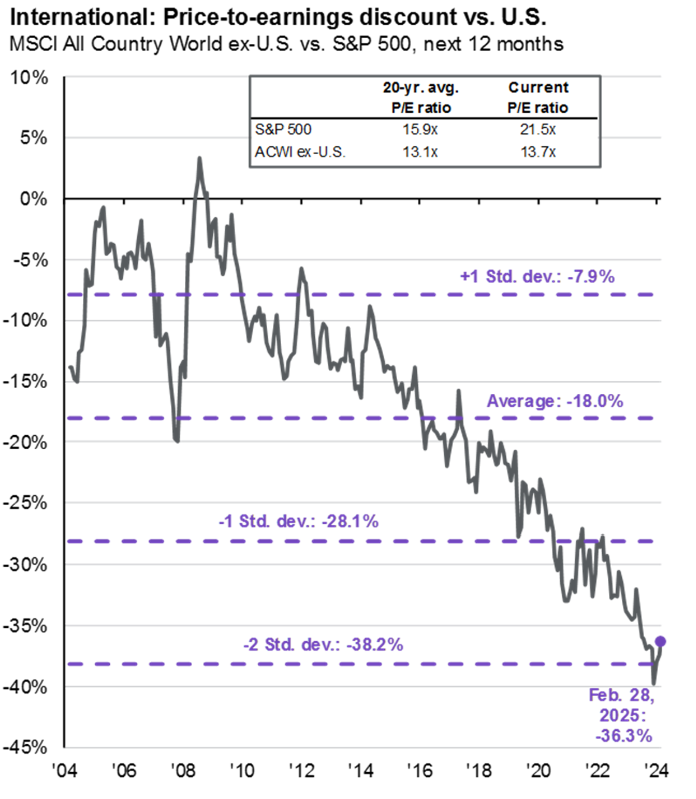

On a longer-term basis, U.S. large cap equities, defined by the S&P 500 Index, has outperformed international equity markets. While not a great investment strategy, many investors use past performance to guide their allocation decisions. With international equity markets underperforming the U.S. market for years, investors may be under-allocated to international relative to where they may otherwise want to be. If investors do want to diversify further into international equity markets, this could put some additional support on foreign equity markets from here.

Another supporting factor for international exposure is valuations. Valuations outside of the U.S. remain attractively below that of U.S. equities. U.S. tariffs are a wild card on foreign countries’ businesses and economies, but the valuation discount to U.S. equities provides some comfort that investors aren’t paying a hefty premium for foreign equity exposure.

In addition, potentially newfound domestic government and citizen support for their own countries on the back of increased geopolitical risk with the U.S. may provide some support for investing in their own countries, or maybe just reducing exposure to the U.S.

I continue to prefer some international equity exposure to both developed and emerging markets. While these areas have generally lagged the last couple of years, I’m ok with it. My diversified exposure to international equities has been helpful this year. I also remain tactically allocated to leveraged Chinese equities (which has been very beneficial) and diversified emerging markets in my Global Unconstrained strategy. If Chinese equities continue to rally a bit more from here, I anticipate selling out of that position as my target has been met.

HIGH INCOME

I continue to like the diversification across higher income-generating asset classes and strategies: option income, credit-sensitive bonds, closed-end funds, dividend growth, tactical income strategies. I don’t know where the Trump administration will ultimately land with their policies, but I am anticipating market upside and downside volatility to continue. If it does, having income generating assets could help provide some support.

As equity markets declined from their highs, a lot of the decline was driven by “growth-ier” stocks, while “value” stocks, low volatility stocks and higher dividend-paying stocks held up better, if not rallied in this environment. As these areas of the market held up better than others, it was a source of “drier powder” for me to take from and reallocate to other areas that had declined more, including to leveraged positions I have on for a couple of the strategies I manage.

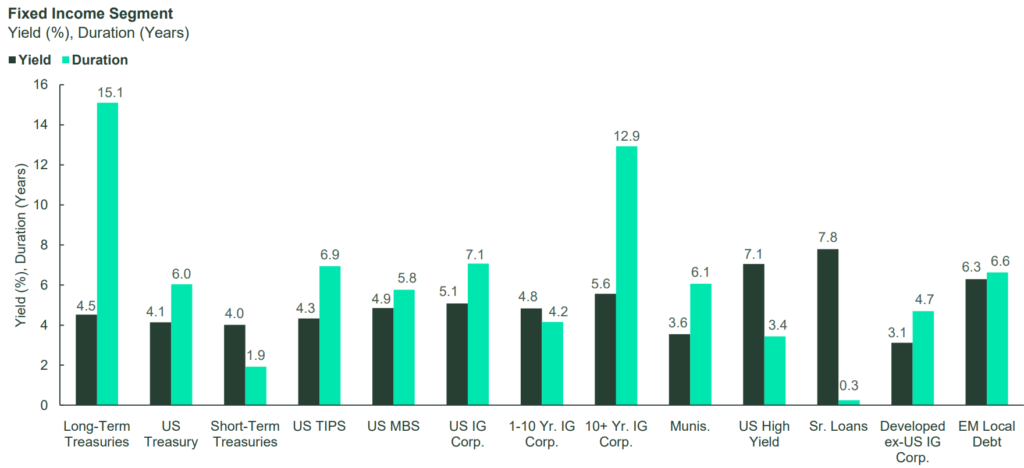

High yield credit spreads have widened a little bit as risk assets have sold off, but they remain tight relative to history. Even with tight spreads, the high absolute yield of below investment grade bonds continue to support my moderately bullish view on high income assets. With U.S. high yield, securitized loans, and emerging markets debt trading at 6-7% yields, those remains attractive to me and I remain allocated to strategies that provide those exposures.

COMMODITIES

I still don’t have a lot of conviction across commodities, but I remain slightly bullish overall.

If the U.S. government leadership can finalize whatever tariff policies they want to implement, that could at least remove an uncertainty overhang. If tariffs don’t have as much as a bite as feared, this could be bullish for global growth. If countries outside of the U.S. decide they want to try to rely less on the U.S. and reinvigorate their own economies, foreign governments may increase spending, drive greater demand for commodities, and commodity prices could move higher.

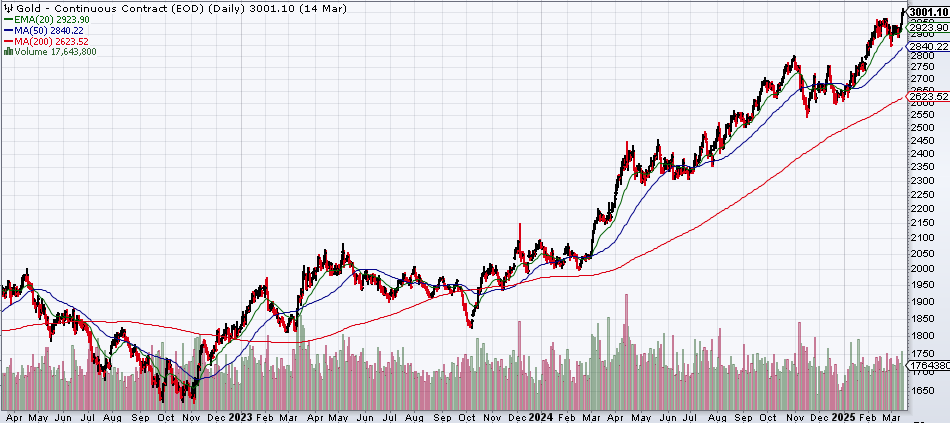

Gold prices continue to be on a rally higher. Market technicals remain strongly bullish, the U.S. dollar has been weak and geopolitical uncertainty persists. Until gold’s market technicals weaken, investors may remain bullish and the price could continue to grind higher.

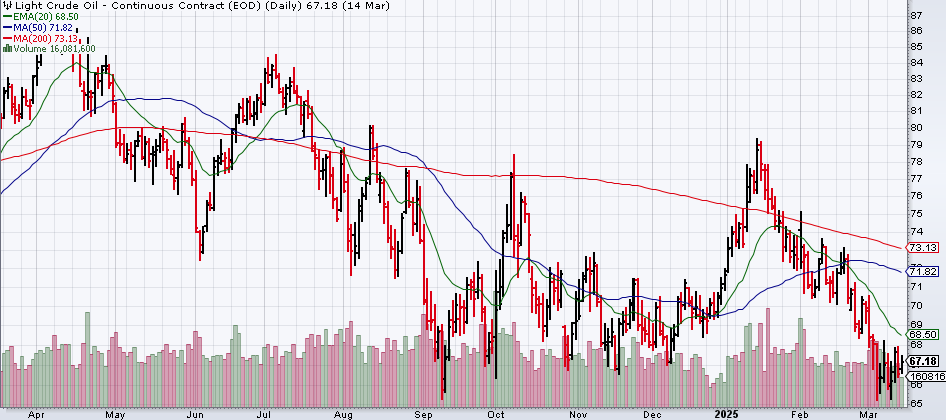

WTI Crude Oil prices have remained volatile. WTI Crude Oil rallied to around $80/bbl to start the year, but it has since sold off to the lows experienced in Q4 last year. The Trump administration continues to support a “drill baby drill” policy, which could keep downward pressure on oil prices, but I personally doubt oil companies want to spend capital on increased oil production in an environment of low oil prices. For this reason, I think oil prices just trade in a wide range as they have been, maybe within the $60-$90 range. We’re closer to the lower end of that range now, so I wouldn’t be overly bearish at these levels.

CONSERVATIVE ASSETS

I remain slightly bullish on conservative assets at these levels.

At the beginning of the year, investors were bullish on the economy but believed that inflationary pressures from potential tariffs under President Trump’s administration could be an issue. As policy uncertainty increased, business and consumer sentiment weakened, investors and economists started getting nervous with their economic growth projections.

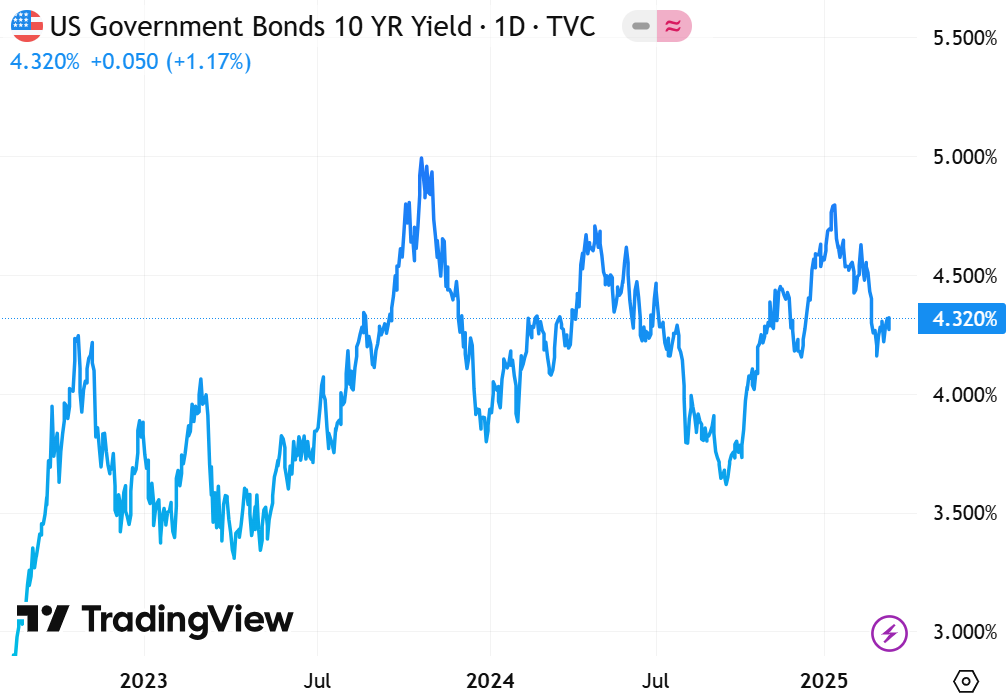

As nervousness increased, investors started to flock to safe-haven assets, including Treasuries. This pushed Treasury yields lower, from above 4.5%-5% across the yield curve, to down to below 4.5%. Investors with exposure to high-quality, interest rate-sensitive bonds have enjoyed a nice rally this year. I have stated I would become increasingly bullish on interest rate-sensitive bonds when the yield curve was above 4.5%, and it was, and I was. Now it’s back below 4.5%, so I’m back to slightly bullish.

Credit spreads remain tight relative to history. While credit spreads have widened a little bit, it is not enough for me to want to take on added credit risk. I need a bigger selloff in credit to want to reduce exposure to safer bonds and allocate to riskier bonds.

If we continue to get a slowdown in economic growth, whether it’s due to the natural economic cycle or driven by fiscal policies, the economic data will show evidence of it. If unemployment starts to tick higher and inflationary pressures subside, the U.S. Federal Reserve may continue to cut the fed funds rate further. The Fed has been consistent in saying they would be focused on the economic data. The Fed is meant to be an independent body and should not be impacted by politics. We’ll just need to keep an eye on the economic data to try to determine what the Fed’s actions might be in the future.

With bond yields remaining attractive at these levels, significant uncertainty continues, and the Fed is anticipated to keep cutting interest rates, I continue to be slightly bullish on conservative assets. To gain diversified exposure to bond markets, I continue to allocate to actively-managed bond strategies that have the flexibility to allocate across bond sectors, credit quality, manage duration/yield curve exposure and take advantage of idiosyncratic opportunities in the bond market.

U.S. GOVERNMENT BONDS

In my previous commentaries, I indicated I would be increasingly bullish on conservative bonds above 4.5% across 10+ year maturities on the yield curve. As you can see from the graph below, that’s what happened. As the yield curve has now shifted below 4.5%, I’m now back to only slightly bullish on conservative assets. If the yield curve continued to decline on growth fears and yields fall closer to 3.5%, I anticipate I would shift to slightly bearish on conservative assets at that time as I believe longer-term rates may need to stay higher due to the high debt levels of the U.S. government.

I believe the U.S. still has a significant issue with trying to manage its outstanding debt that continues to grow. To get it under control, we may need more government spending cuts and higher taxes. Both are headwinds to economic growth. Unless we see material action to reign in the U.S. deficit and tackle outstanding debt, long-term interest rates on U.S. Treasuries could continue to move higher. In this scenario, interest rate-sensitive Treasuries and other bonds could experience downward price pressures.

U.S. INVESTMENT GRADE CREDIT

I maintain my slightly bullish view on U.S. investment grade credit at this time.

Corporate bond spreads remain tight and at the lower end of the historical range, although spreads have widened slightly as risk assets have declined. I need to see credit spreads a lot wider than they are now in order to consider increasing my bullish positioning on U.S. investment grade credit.

The absolute yields in credit remain attractive and credit-sensitive bonds can still act as a potential “safer haven” relative to equities if economic and corporate growth becomes weaker than expected.

OTHER

I use this section to talk about other potential strategies, generally whether or not hedges are needed on asset classes.

I remain slightly bullish on hedges to risk assets at this time. With lack of fiscal clarity on tariffs, government spending cuts, the final tax legislation and what appears to be increased global rhetoric against the U.S., uncertainty remains.

For conservative investors looking for non-traditional investment strategies to hedge their portfolios, this could still be a time to maintain some hedges. Bonds continue to generate attractive yields and could be the safe-haven assets investors seek if equity markets continue to experience weakness.

For me, and particularly after the recent selloff in U.S. equities, I prefer my diversification across asset classes and higher income-generating assets to help reduce volatility in my portfolios. I prefer not to utilize tactical, hedged equity strategies in this environment and prefer traditional higher income-generating assets to act as my “drier powder” instead.